if GetSymbolInfo("買賣現沖")=false or GetSymbolInfo("處置股")=true then raiseruntimeerror("不可當沖");

///變數定義

variable:flag(0),_low(0),_low2(0),barcount(0),flag1bar(0),flag2bar(0),flag3bar(0),flag4bar(0),flag1count(0),flag4count(0),flag5count(0)

,flag6count(0),_sellcount(0),_low11(0),_lowperiod2(0),_periodhigh2(0),_period2(0),flag7count(0),_highperiodtime(0),_highperiodtime2(0),

recordhigh(0),arecord(0),alow(0),condition3_(0),AAA(0),barcount1(0),M(0),_sellprice(0),_switch(0),positioncount(0),

volumeflag1(0),flag1highvolumebar(0),i(0),tv(0),tp(0),close2(0),_high2(0),_true(0),highcount(0),volhigh(0),vollowprice(0),volhigh2(0),_period(0),_periodhigh(0),_lowperiod(0);

VARiable:INTRaBarPersist flagnum(0),_high(0);

//////////////////////////////////////////////////////////////////////////選股邏輯//////////////////////////////////////////////////////////////////////

///barcount 定義///

if date <> date[1] then ///參數定義

begin

barcount=1;

end

else

barcount+=1;

////////////////////////////////////////////////////////判斷價位區間

if c>10 and c<20 then _switch=10;

if c>20 and c<30 then _switch=20;

if c>30 and c<40 then _switch=30;

if c>40 and c<50 then _switch=40;

if c>50 and c<60 then _switch=50;

if c>60 and c<70 then _switch=60;

if c>70 and c<80 then _switch=70;

if c>80 and c<90 then _switch=80;

if c>90 and c<100 then _switch=90;

if c>100 then _switch=100;

///下單張數

positioncount=Round(300/c,0);

//////////////////////////////////////////////////////////////////////////////////進場條件////////////////////////////////////////////////////////////

//////////////////////////////

if c>_avgprice and GetField("成交量", "D")[1]>500 and _estvolume99>4

then begin

setposition(1);

end;

print(file("C:\print\"),date,barcount,position,c,_avgprice,GetField("成交量", "D")[1],_estvolume99);

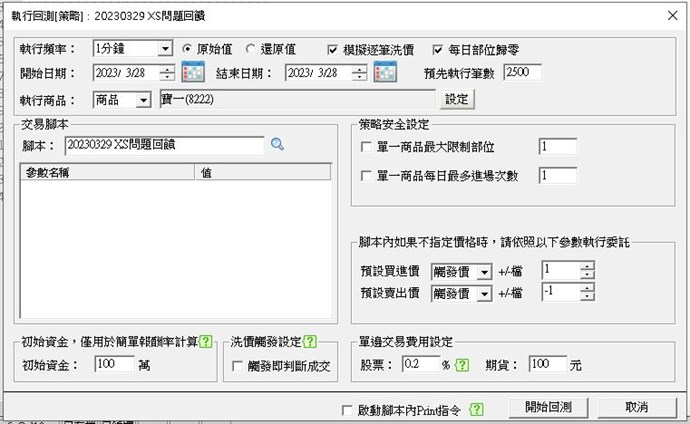

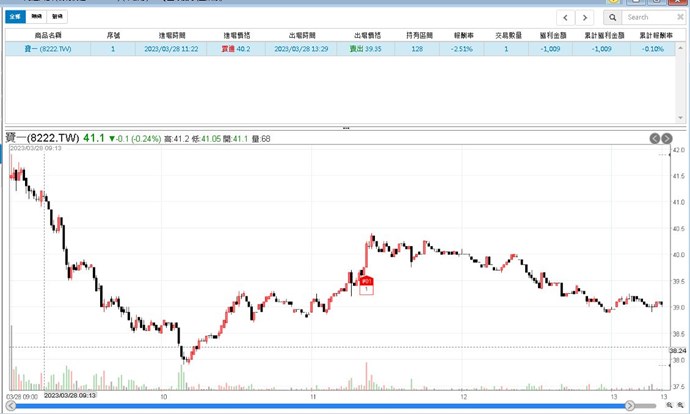

以上為程式碼,以下為print出來的結果

可以看到其中一項進場條件為_estvolume99>4才進場,可是print出來看只有0.6多

卻觸發進場,今天盤中開起來自動交易模擬有進場 回測結果也是如此

請問小幫手這個情況該怎麼解決?

date, barcount, position, c, _avgprice , GetField("成交量", "D")[1], _estvolume99

20230328.000000 143.000000 0.000000 40.250000 39.772378 48104.000000 0.642940

20230328.000000 143.000000 1.000000 40.200000 39.773384 48104.000000 0.648012

20230328.000000 144.000000 1.000000 40.150000 39.774456 48104.000000 0.648552

5 評論